Is This the Start of an Oil Bull Run?

Oil prices spiked 7% on Friday following dramatic escalations in the Middle East. But is this the beginning of a sustained bull run, or just another geopolitical head fake?

What Happened?

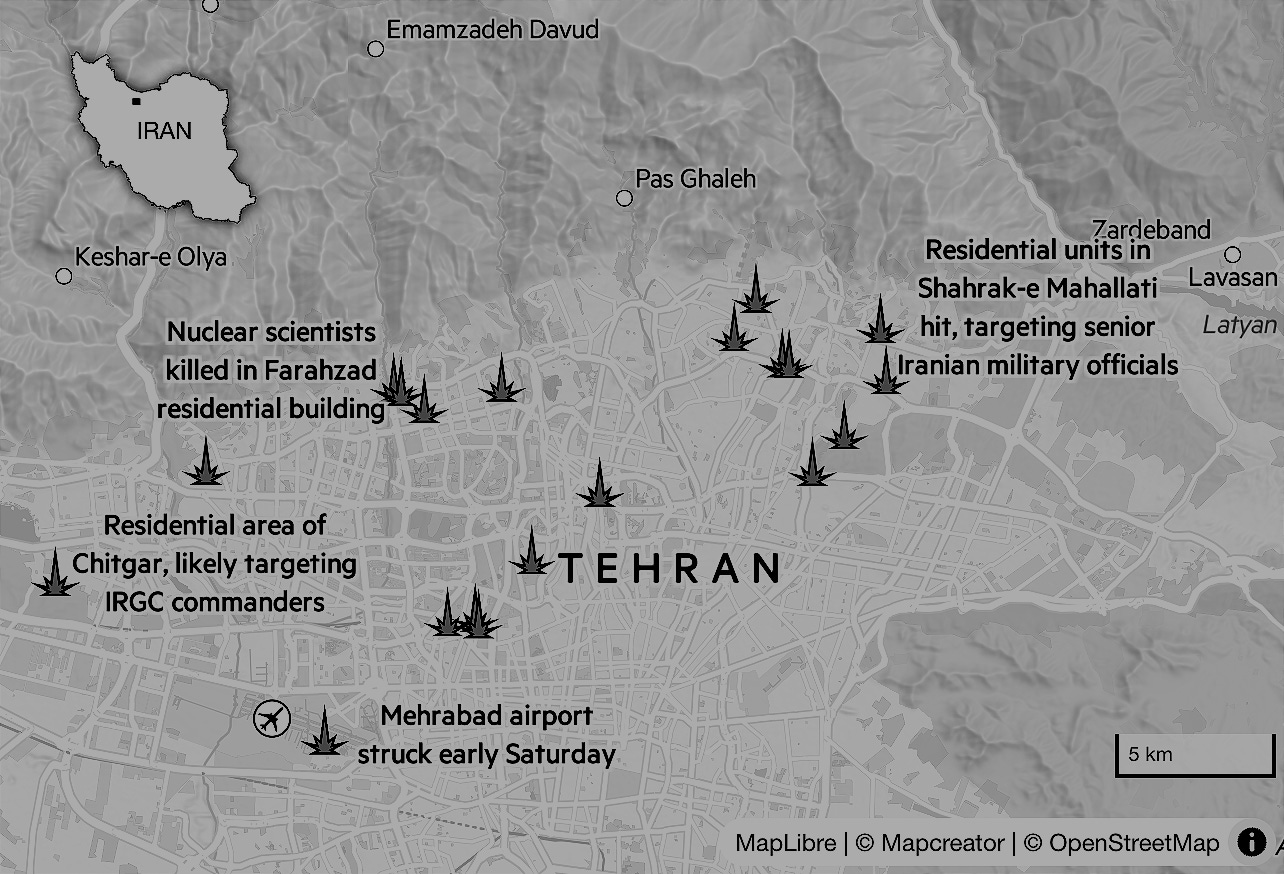

On Friday, Israel launched a coordinated attack against Iran, targeting ~100 sites, including nuclear sites, military bases, weapons facilities, and residential compounds:

Iran’s foreign ministry quickly blamed the Trump administration for coordinating with Israel, declaring that Sunday’s scheduled nuclear talks with the U.S. were now “meaningless.” Officials claimed the peace process had been derailed, and warned of retaliation.

A few hours later, Iran reportedly struck a target in Central Israel. Two people were killed and 19 injured. This image circulated on X:

Brigadier General Ahmad Vahidi stated the strikes hit 150 targets, promising the operation would "continue as long as necessary" and that “this is just the beginning.”

Oil markets initially surged, with WTI crude jumping as much as 13% intraday, before closing Friday up 7%:

Traders on X, particularly those on the technical or chartist side, seem to believe that this move ignited a larger incoming increase, and many have already begun calling for prices as high as $130 to even $300 per barrel.

Over the weekend, rumors began to circulate that Iran had closed the Strait of Hormuz, a key chokepoint through which 20% of global oil shipments pass. Our research suggests these claims are false. While Iran has historically threatened to close the strait during periods of tension, it remains open. The waters belong to Oman, anyway. And geopolitically, a full closure would hurt Iran as much as it would hurt the West:

In 2024, about 1.35 million barrels per day of Iranian crude and condensate were shipped to China via the Strait of Hormuz, which is by far the largest buyer of Iranian oil, absorbing more than 95% of Iran’s oil exports. A closure would block this route, forcing Iran to rely on the Goreh-Jask pipeline to the Sea of Oman. However, this pipeline’s capacity is limited to 300,000–1 million barrels per day, creating a significant shortfall. Given Iran’s growing military expenditures and financial pressures, maintaining uninterrupted exports, in our view, is essential:

Either way, a short-term spike in oil prices is, of course, a possibility. But such a move would be backed entirely by geopolitics, and almost no one ever made money speculating on geopolitics with oil futures. Over the longer term, oil prices are highly sensitive to the economy and serve as a real-time indicator of economic health.

The Bigger Picture

With soft oil prices in combination with less drilling activity (US oil rig count), oil tells us that we are (already) in a period of economic slowdown:

Nothing about this chart is healthy or bullish for the near term as it shows the opposite of what we would like to see in a bullish economic environment. Rather, we believe that it reinforces our belief that we are in a stagflationary period: slowing growth, sticky inflation, and weak commodity demand. Under these conditions, it is unlikely that oil prices can sustain a meaningful bull run.

In the near term, while there could be temporary spikes due to further escalations, we project the oil prices to remain soft. Over the medium to long term, low prices cure low prices. It may take 3–5 years, but the supply-demand imbalance will correct. In the meantime, quality matters: high quality producers like Exxon Mobil and Canadian Natural remain profitable at current prices. Our favorite royalty play, Freehold Royalties, also promises strong free cash flow, even at $45 oil.

Therefore, despite our neutral/bearish outlook for the very near term, we continue to own and accumulate CNQ 0.00%↑ and $FRU.TO and are looking to possibly enter a long position in Exxon once the situation in the middle east cools down. Note that we are going to hold these positions for multiple years and we cannot guarantee positive returns this year.

Final Thoughts

The headlines are loud, and the charts are getting passed around like candy on X. But make no mistake, this kind of spike has happened before, and it usually fades just as fast. Oil is currently reacting to fear, not fundamentals. And while fear can move prices, it doesn't build sustainable trends. If anything, oil is telling us a very different story; one of slowdown and capital discipline.

For a real bull market to take hold, we’d need to see economic strength, rising demand, and an uptick in drilling. Right now, we’re not seeing any of that.

So for now, we’re not chasing spikes. We’re holding quality names that can weather the storm. Markets reward patience.

Thank you for reading. If you found this useful, please subscribe below. It’s FREE. We’ll keep sharing what we’re seeing; no hype and no BS.

— Antithesis